Just wanting confirm when I complete a backtest on a universe of stocks using the Monthly Rank function such as ARR(), I can also add a secondary rank formula such as Performance().

The results adding a secondary rank formula differ quite abit - is this because these are being double sorted or a layered rank? How can we replicate this process in the backtest double rank in real life to mimic this strategy.

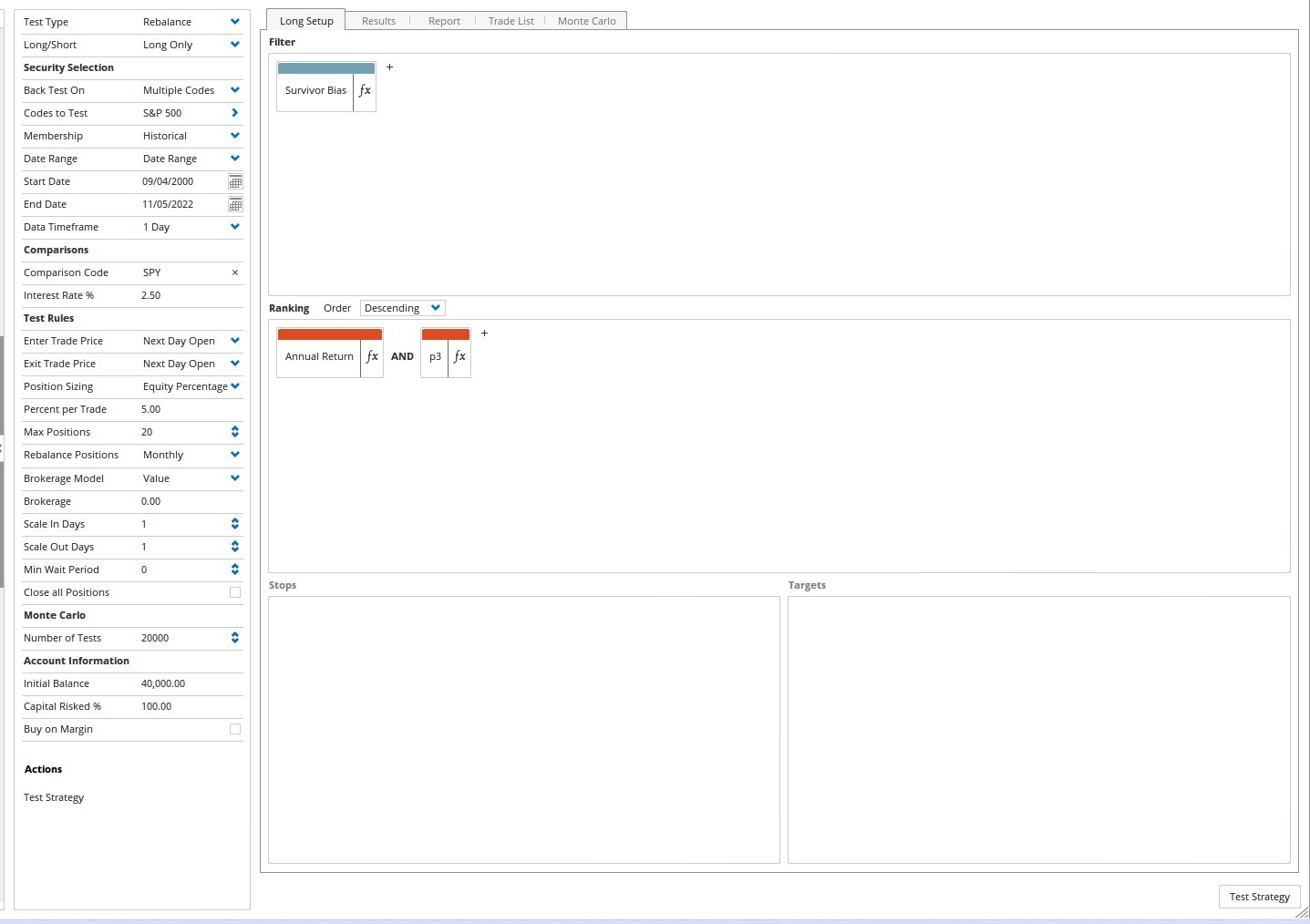

I am not 100% sure what it is you are doing in the setup. If you could please send a copy of the back test file to [email protected] with a screen shot reference, we can look into more detail there.

For some reason the workbook isnt sending - however here is the screenshot of the test. First criteria is ARR() and the second is performance(PERIODAMT=3). Wanting to understand if this is a legitimate test and/or if its possible to replicate in replicate in real life.