I am working on backtests with yield-oriented stocks and want to ensure I am doing it correctly.

Is it as simple as using the price adjustment below and running the backtest off that within the script?

Or are there any adjustments to the script that need to be made when working with total return data? IE, I have seen other references to using TRET(), etc.

That’s the same as using TRET() CrossesAbove TRET()[10] if running the test on the same symbol.

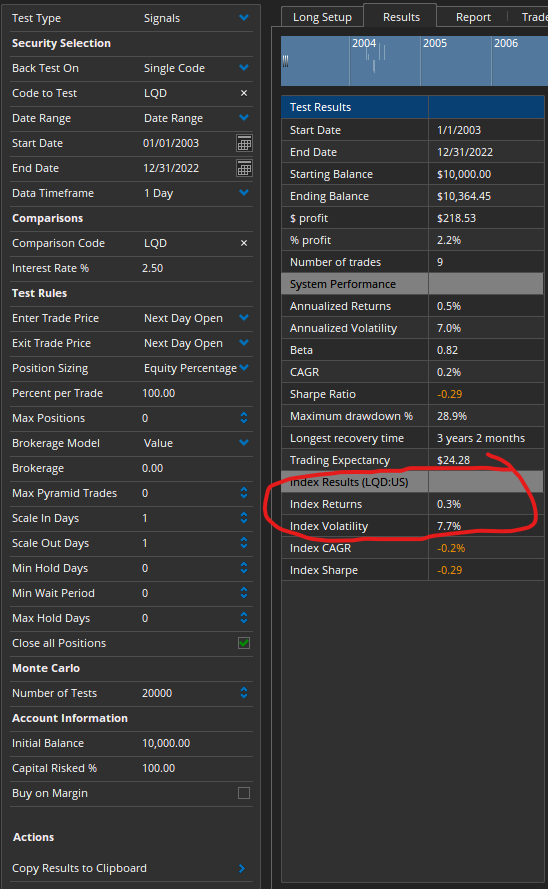

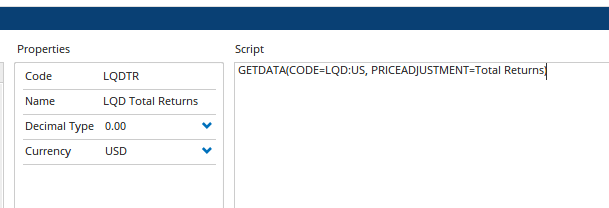

Yes index results are price returns (the new tester will have total returns) but there is a workaround… under Data > Custom Codes create a new symbol (eg LQDTR) using the GETDATA() formula: